I will give an overview of the swap rates and how this is constructed from the implied forward and spot rates.

First, we need Depo’s and EuroDollar futures which are liquid and exchange traded instruments from which the

Now to the next section, we need to price swap, lets say 1Y2Y swap. First, we need to get the 2 year swap rate for which we need to value both legs to zero. The answer is the “average” of the first two years of the forward curve, specifically the sequence of forward rates on 3-month LIBOR.

In general market makers set the bid and ask rates on over-the-counter (OTC) derivatives such as forwards and swaps based on the cost and risk of the most efficient way of hedging risk. When available, actively traded futures contract offer the best hedge. Note that main difference between forward and futures is settling arrangement. Whereas forward are settled as per contract agreement on the expiry dates, futures are daily settled and margins accrued typically every day.

Why is the forward interest rate lower than the otherwise comparable futures rate? The key is that the gains and losses on an OTC forward contract are realized in a lump sum at the delivery date.

is given by,

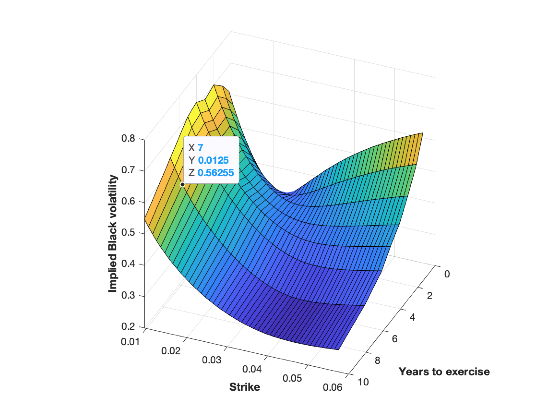

is given by,![\sigma_{ATM} = \frac{\alpha_0}{f^{1-\beta}}\{ 1 + [\frac{(1-\beta)^2}{24}\frac{\alpha_0^2}{f^{2-2\beta}} + \frac{\rho \beta \nu \alpha_0}{4 f^{1-\beta}} + \frac {2 -3\rho^2}{24} \nu^2] T \}](https://s0.wp.com/latex.php?latex=%5Csigma_%7BATM%7D+%3D+%5Cfrac%7B%5Calpha_0%7D%7Bf%5E%7B1-%5Cbeta%7D%7D%5C%7B+1+%2B+%5B%5Cfrac%7B%281-%5Cbeta%29%5E2%7D%7B24%7D%5Cfrac%7B%5Calpha_0%5E2%7D%7Bf%5E%7B2-2%5Cbeta%7D%7D++%2B+%5Cfrac%7B%5Crho+%5Cbeta+%5Cnu+%5Calpha_0%7D%7B4+f%5E%7B1-%5Cbeta%7D%7D++%2B+%5Cfrac+%7B2+-3%5Crho%5E2%7D%7B24%7D+%5Cnu%5E2%5D+T+%5C%7D&bg=ffffff&fg=000000&s=0&c=20201002)

. Applying them,

. Applying them,

, therefore,

, therefore,  . We now apply,

. We now apply,

, so applying, we get the final derivation,

, so applying, we get the final derivation,

, where

, where

![E_t = A_t [ N(d_1) + L N(d_2) ]](https://s0.wp.com/latex.php?latex=E_t++%3D+A_t+%5B+N%28d_1%29+%2B+L+N%28d_2%29+%5D+&bg=ffffff&fg=000000&s=0&c=20201002)

![CVA = LGD (PD_{(0, T)}) D_{(0, T)} E[max(V_j,0)^+]](https://s0.wp.com/latex.php?latex=CVA+%3D+LGD+%28PD_%7B%280%2C+T%29%7D%29+D_%7B%280%2C+T%29%7D+E%5Bmax%28V_j%2C0%29%5E%2B%5D+&bg=ffffff&fg=000000&s=0&c=20201002)